Ripple paid remittances firm MoneyGram $9.3 million in XRP incentives during the third quarter of 2020.

MoneyGram revealed the figure in its earnings report released on Thursday. The Nasdaq-listed firm said Ripple paid $9.3 million, but $400,000 was offset by related transaction and trading expenses, leaving $8.9 million as a net benefit.

MoneyGram categorizes these payouts as “market development fees” rather than revenue. The firm gets paid based on transaction volume it processes via Ripple’s On-Demand Liquidity (ODL) product that utilizes XRP for settlements.

Compared with the previous quarter, MoneyGram received $5.8 million lesser from Ripple in Q3, suggesting that the money transfer firm processed fewer payments in XRP in the latest quarter.

Ripple and MoneyGram partnered in June 2019 to leverage XRP in forex settlements as part of MoneyGram’s cross-border payment process. As part of the deal, Ripple invested $50 million in MoneyGram. Their partnership agreement is scheduled to expire in July 2023.

While MoneyGram receives incentives in XRP, the firm does not hold the digital asset. “We sell XRP as soon as we receive it,” a MoneyGram spokesperson told The Block earlier this year.

Crypto lending and trading firm Genesis continues to grow.

The firm issued $5.2 billion worth of new loans in the third quarter of 2020, more than double its previous record of $2.2 billion in Q2, according to a report shared with The Block on Friday.

Genesis began its lending business in March 2018 and since then has originated $13.6 billion worth of loans in total. The recent growth came through increased cash and altcoin loan issuance, said Genesis, along with a “modest” increase in the notional value of crypto loans outstanding. Genesis’ active loans outstanding grew 50% in Q3 to $2.1 billion, compared to $1.4 billion in the previous quarter. Outstanding loans are balances that borrowers are obligated to repay. As Genesis facilitates lending, it also lets others lend via its platform. As of September 30, 2020, Genesis had 165 unique lenders, up 47.3% from the previous quarter. “September’s monthly total interest payout represented over 20% of all interest paid in the trailing 12-month period,” said the firm.

Genesis further said that growth in banks’ deposits is also helping it. “Banks must make loans somewhere; prime brokerage clients are great places to deploy excess capital during a pandemic. These clients have historically worked closely with Genesis and are now lending both excess USD and BTC generated from the short CME basis trade back to Genesis, ultimately increasing our asset base as well,” explained the firm.

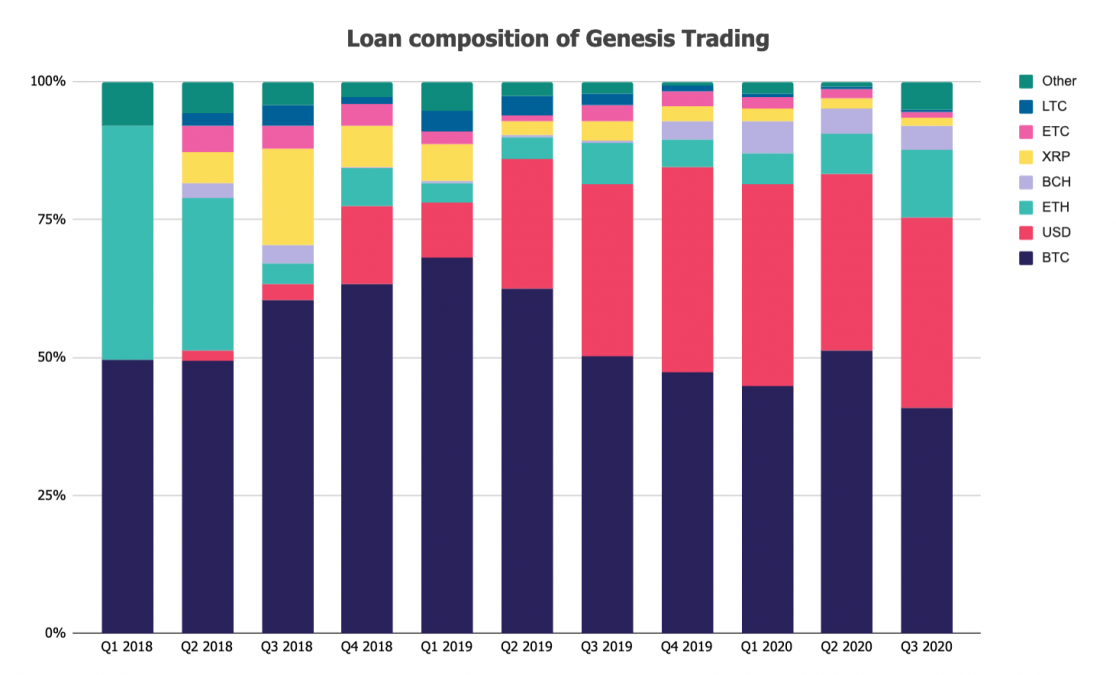

Share of BTC declined

Altcoins and the U.S. dollar drove Genesis’ loan portfolio in Q3, not bitcoin (BTC). The firm’s BTC composition as a percentage of loans outstanding fell sharply in Q3 to 40.8% as compared to 51.2% in the previous quarter.

“ETH, USD and Equivalents and ‘other’ altcoins drove the increase in book size in Q3,” said Genesis. “ETH loans outstanding jumped to 12.4% of the overall book, USD increased to 34.5%, and other altcoins jumped to almost 5.0%.”

The main driver of this portfolio shift came from the decentralized finance (DeFi) boom, according to Genesis, which said, “our trading counterparties started actively borrowing ETH and stablecoins to lever up liquidity mining strategies.”

Genesis also facilitates spot and derivatives trading and these businesses also grew significantly in Q3. The firm recorded a $4.5 billion volume on the spot trading side, up 285% from the same quarter in 2019. On the derivative trading side, Genesis recorded $1 billion in total volume, up from $400 million in Q2 when it launched its derivatives trading business.

While Genesis facilitates most customer trades via its over-the-counter (OTC) desk, the firm said it had seen consistent growth in electronic execution. In September, Genesis executed almost 30% of all spot trading volume through its new Prime smart-order routing engine, the firm said.

One of the most unfortunate aspects of the crypto space is its tendency to attract scams. The world bore witness to this in early July when one of the boldest hacks in Internet history – the hijacking of several prominent Twitter accounts, including those of presidential candidate Joe Biden as well as tech titans Bill Gates and Jeff Bezos – turned out to be a ruse to harvest some bitcoin.

CoinDesk was one of the hijacked accounts, too (our handle is all better now, thanks), and it was far from the first time our brand was exploited by crooks looking to make a quick buck. Nor has it been the last.

Previously, scammers impersonated CoinDesk reporters on Telegram and other networks, typically promising coverage in exchange for payment (something we would never do).

Now, some enterprising hoodlums have taken their tricks to a new level.

Over the past few weeks, CoinDesk has seen evidence scammers are copying our newsletters in their entirety, adding a malicious link at the top and changing the subject line to emphasize that link. They then send the email to a list of active and perhaps crypto-curious email addresses likely acquired from privacy-ignoring data brokers or the dark web, completing the phishing scheme.

This is maddening to both us and the victims, since often they never signed up for the mailings in the first place. When they attempt to unsubscribe from the email, they’re either taken to a link that doesn’t work or worse – pulled into the phisher’s trap yet again.

A telltale sign

Admittedly, it can be hard to tell the difference between one of our legit newsletters and one of these phishing copies. The fonts are wrong – but if you’ve never subscribed, how would you know?

There is a giveaway but you need to be paying attention: The malicious link is often in a short “news” item that comes right after the byline, usually touting a company you’ve never heard of.

None of our newsletters begin this way, so if you see one of these, flag it right away by forwarding the email to fraud@coindesk.com.

Compare one fake email we were forwarded…

…to the genuine article:

Rest assured we’re working to identify these scammers so they pay for their crimes (and they are crimes) as well as upgrading our newsletter experiences to improve security.

In the meantime, be sure to practice good inbox management: Be wary of suspicious-looking links; block or filter senders instead of clicking on unsubscribe buttons; and remember, absolutely no one is going to send you back double your bitcoin. Not even your mom.

Not an exchange

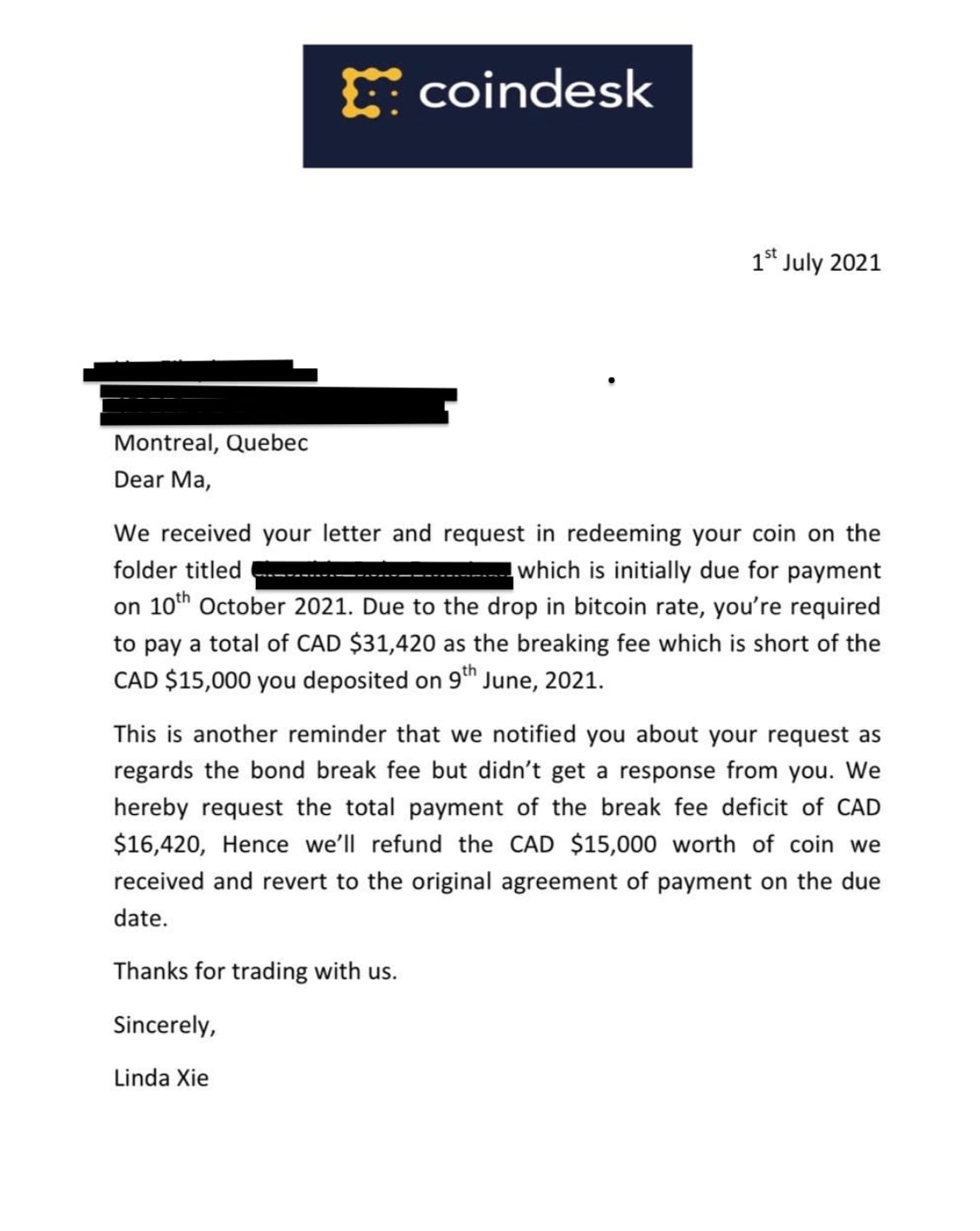

CoinDesk is often confused with Coinbase, the popular cryptocurrency exchange, and in July 2021 a scammer apparently tried to take advantage of this by sending the following email bearing our logo to a hapless Canadian:

To be clear: CoinDesk is a media and events company, not a crypto exchange. No one trades with us.

There is no Linda Xie at CoinDesk. The phishers may have been impersonating a former Coinbase executive by that name.

The grammatical errors were a red flag. Another is that the email was sent from a Gmail address. Any legitimate email from a CoinDesk staffer would come from an “@CoinDesk.com” address.

Unfortunately, the recipient still fell for the ruse and sent the phishers $17,000, according to a subsequent email the victim received which CoinDesk reviewed. (Subject line: “Fault and bridge [sic] of contract warning.”)

If you or someone you know receives an email resembling the one above, DO NOT SEND ANY MONEY. Again, forward any suspicious messages to fraud@coindesk.com.

UPDATE (Oct. 26, 2021, 01:15 UTC): Adds section at bottom about recent email scam.

Fidelity Digital Assets collaborated with Greenwich Associates to survey almost 800 investors in order to produce a deeper understanding of the preferences of major institutions and their behavior toward the digital assets industry.

Delphi Digital takes a close look at bitcoin’s metrics and evolution as macro policies set the stage for currency debasement and as the halving changes the economics of bitcoin mining.

Since its introduction in 2009, Bitcoin has steadily grown in popularity and today has expanded its reach to a broad mainstream audience. A joint survey from Grayscale Investments and Q8 Research provides a deeper level of insight into investors’ interests, perceptions, and misconceptions about investing in Bitcoin including the profile of potential Bitcoin investors, the messages that drive Bitcoin’s appeal, and investor sentiment around Bitcoin vs. gold.

CoinDesk Research covers crypto markets quarterly data including volatility, correlation, volume and returns of the CoinDesk 20 list of crypto assets. This quarter’s slides also cover derivatives markets, synthetic bitcoins, BTC versus ETH, central bank digital currencies and the return of aging bitcoin mining equipment; finally, we look at the relationship (or not) between online sports betting and crypto markets.

In May of 2020, bitcoin is expected to undergo its third “halving,” a programmed supply reduction that has in the past coincided with a strong run-up in the bitcoin price. In this paper, we explain what the bitcoin halving is, why it matters and why the market is so focused on this event. We attempt to reconcile the various models and theses around the potential bitcoin price reaction as the adjustment approaches, and look at metrics that will shed light on the technological impact. We finish with some input from miners themselves, who lend insight and perspective to the possible consequences of the protocol change.

A newly proposed Ethereum hard fork may punt a key network feature two years down the road to avoid complicating Ethereum’s transition to proof-of-stake (PoS).

Ethereum improvement proposal (EIP) 2387, created in mid-November, would tentatively schedule a Jan. 6 hard fork to delay the “difficulty bomb” or “Ice Age” from going off for another 4,000,000 blocks or about 611 days. The hard fork is dubbed “Muir Glacier,” after the retreating Alaskan glacier.

Slated for block number 9,069,000, the hard fork contains a bridge between the current chain, based on a proof-of-work (PoW) consensus mechanism, and the Beacon Chain, or the first phase of the so-called Eth 2.0 transition to PoS.

With other networks like EOS, Binance Chain and Substrate looking to pick off projects from Ethereum, developers voiced concerns on a call last Friday over maintaining the current chain’s health as the transition to Eth 2.0 occurs. Complicating matters, the network’s next major hard fork, Istanbul, is now slated for Saturday.

If developers fail to agree on Muir Glacier soon, which remains unlikely after reaching rough consensus on a developer call last week, block times will continue to move upward, restricting the current network’s capabilities as transaction fees crowd out users.

The difficulty bomb, explained

A piece of code embedded in 2015, the difficulty bomb is one of two components which gradually increases the hashing difficulty on the Ethereum blockchain, meant to force the network towards PoS with the Serenity network overhaul, currently slated for 2021.

Similar to Bitcoin, Ethereum features a mining difficulty adjustment scheme to control the output of ether rewards for mining on the network, which the bomb is a part of.

Unlike Bitcoin, Ethereum’s pending difficulty bomb will increase the time it takes to mine a block – typically between 10 and 20 seconds – every 100,000 blocks. Since the difficulty bomb is based on when blocks are mined, knowing when the network will feel the effects is more art than science.

EIP 2387 would be the third time since 2015 the bomb’s fuse has been extended, first by 3 million blocks in the 2018 Byzantium hard fork and then by another 2 million blocks in the February 2019 Constantinople hard fork.

Source: TrueBlocks, LLC

High settlement times are not alien to Ethereum. As data provider Etherscan shows, block times soared before both the Byzantium and Constantinople hard forks, hitting over 30 and 20 seconds, respectively.

Source: Etherscan.io

“It looks like given faster block times since Constantinople, it was a bit underestimated on when [high transaction fees] would hit again,” Ethereum developer Eric Conner said in a private message. “People were under the assumption we had until the next fork after Istanbul, but actually it’s slowly kicking in now.”

In light of the earlier-than-expected uptick, Conner drafted EIP 2384, the Istanbul/Berlin Difficulty Bomb Delay, included in EIP 2387. In a little over six weeks, block times have increased from 13.1 to 14.3 seconds, Conner said. And, as the difficulty bomb is an exponential feature of Ethereum, a one-second change has large implications down the road.

Keeping up with the network

Although the difficulty bomb is an original feature of Ethereum, some developers have called for getting rid it altogether. After all, its launch has been punted every time it becomes inconvenient.

Some see the logic in maintaining the original design, however. It does force Ethereum clients to stay on top of updates or face increasing costs to run on the network.

“The strongest argument for keeping some kind of expiry is to ensure that there is no option for ‘do nothing,’” Ethereum developer Micah Zoltu said in a private message.

“The issue is more around stakeholders just simply no longer paying attention and not upgrading their clients,” he said. “The bomb is about ensuring people have to make a conscious decision to fork in the face of regular network upgrades.”

For now, EIP 2384 currently stands on last call for comment among Ethereum developers. EIP 2387 reached rough consensus in last Friday’s call, but awaits both finalization of EIP 2384 and acceptance by Ethereum clients such as Parity or Geth before network implementation.

“I’m on the fence between cutting out the bomb entirely and just changing the way the bomb works,” Zoltu said. “What I’m against is keeping the bomb implemented as it is.”

Genesis’ active loans outstanding grew 50% in Q3 to $2.1 billion, compared to $1.4 billion in the previous quarter. Outstanding loans are balances that borrowers are obligated to repay.

Genesis’ active loans outstanding grew 50% in Q3 to $2.1 billion, compared to $1.4 billion in the previous quarter. Outstanding loans are balances that borrowers are obligated to repay. As Genesis facilitates lending, it also lets others lend via its platform. As of September 30, 2020, Genesis had 165 unique lenders, up 47.3% from the previous quarter. “September’s monthly total interest payout represented over 20% of all interest paid in the trailing 12-month period,” said the firm.

As Genesis facilitates lending, it also lets others lend via its platform. As of September 30, 2020, Genesis had 165 unique lenders, up 47.3% from the previous quarter. “September’s monthly total interest payout represented over 20% of all interest paid in the trailing 12-month period,” said the firm. The main driver of this portfolio shift came from the decentralized finance (DeFi) boom, according to Genesis, which said, “our trading counterparties started actively borrowing ETH and stablecoins to lever up liquidity mining strategies.”

The main driver of this portfolio shift came from the decentralized finance (DeFi) boom, according to Genesis, which said, “our trading counterparties started actively borrowing ETH and stablecoins to lever up liquidity mining strategies.”