Beleaguered crypto lender Celsius has claimed a $1.2 billion hole in its balance sheet, according to new documents filed as part of its newly declared Chapter 11 bankruptcy in New York.

Chapter 11 bankruptcy allows a company to continue operations while meeting its obligations to indebted parties. This is usually executed by proposing a plan of reorganization to be approved by creditors and overseen by a legal team.

The documents, filed on Thursday by CEO Alex Mashinsky and the company’s law firm Kirkland & Ellis, show that the official committee of unsecured creditors likely includes “mostly users.” The firm reported $5.5 billion in total liabilities and $4.3 billion in assets.

Source: Mashinsky court filing

The company said has worked to “unwind” most of its open loans and cease asset deployment services until further notice before commencing with the filing of Chapter 11. It chose to do this due to the volatility of the crypto market.

As of the petition date, the company has unwound nearly all of its DeFi loans and what it called “the FTX loan,” with only one loan remaining in an amount of approximately $3.2 million collateralized by $6.6 million in digital assets, it said.

As of July 10, the company held 410,421 staked ETH (stETH), and as a result, approximately $467 million of the Company’s ETH, based on the market value of ETH, is illiquid, but is earning an approximate 5% APY pending the Merge, it added.

The documents also state that on June 27, 2022, crypto hedge fund Three Arrows Capital (3AC) was ordered by a court in the British Virgin Islands to commence liquidation proceedings.

According to the filing, Celsius has a $40 million claim against 3AC, which, it said is “significantly less than the amount some other companies in the industry, such as Voyager, BlockFi and Blockchain.com, have against 3AC.”

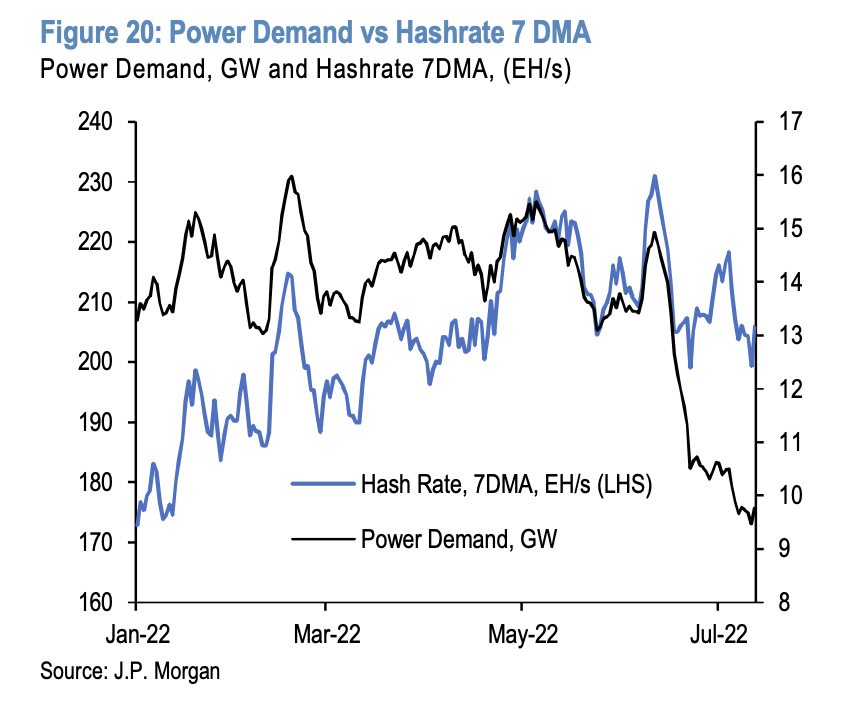

Apart from its main business, Celsius also mines bitcoin through its subsidiary Celsius Mining, which took out up to $750 million in intercompany credit from Celsius. As of May 31, the outstanding balance on that loan was $576 million.

According to the document, Celsius believes that the mining operations will generate enough assets to pay off the loan and “provide revenue for the company in the future.” Celsius owns $720 million in “mining assets,” according to the document.

That side of the business is producing 14.2 BTC a day, which translates to around $292,520 based on bitcoin’s current price of around $20,600, according to TradingView.

The context

Founded in 2017 by Alex Mashinsky and Daniel Leon, Celsius offered retail investors attractive returns on their crypto holdings under the slogan “unbank yourself.” The company, which moved its headquarters from London to New Jersey last year, had grown to manage more than $10 billion in assets and claimed more than 1.7 million users.

© 2022 The Block Crypto, Inc. All Rights Reserved. This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.